The following is the introduction to a new paper by Niskanen Senior Fellow Monica Prasad. Find the full paper below.

The more a government spends on social insurance, the less likely households are to fall into debt. Social insurance includes pensions, health care, family allowances and parental leave, job training, income support, unemployment spending, and other such policies. Spending on these policies enables households to build up assets and reduce debt.

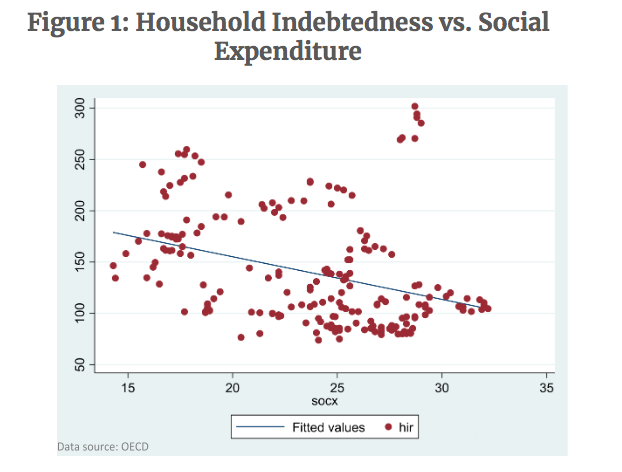

Figure 1 shows this relationship for the years 2007 to 2018 using data from the Organization for Economic Cooperation and Development. On the x-axis is the OECD’s measure of social expenditure (socx) and on the y-axis is the OECD’s household indebtedness ratio (hir), which is households’ debt as a proportion of their assets. Each dot represents one country for one year, and the overall picture is clear: as social expenditure goes up, household indebtedness goes down.

Analysts have been pointing to this trade-off between credit and social insurance for decades. In an important early examination, Teresa Sullivan, Elizabeth Warren, and Jay Westbrook noted that consumer credit is more easily available in the United States, and bankruptcy law is also more lenient to debtors, which serves as a counterbalance to the less extensive social safety net: “The United States offers families more sanctuary in bankruptcy — at the same time that it permits a wide-open consumer credit economy coupled with less protection from the economic consequences of other problems such as job losses, medical problems, accidents, and family breakups. … The European and Canadian approaches, by contrast, make the game safer — but less competitive” by making credit access and bankruptcy more difficult, but by providing extensive social safety nets. All systems do something for families that are struggling to make ends meet: European systems subsidize them more through the social insurance system, while the United States allows them to borrow money and declare bankruptcy more easily. This relationship between credit and the welfare state can be seen in data for the longer period from 1980 to 2005 as well, and it holds even if we control for other factors that influence credit and the development of welfare states, such as economic growth, inflation, unemployment, demographic factors, and the level of interest rates.

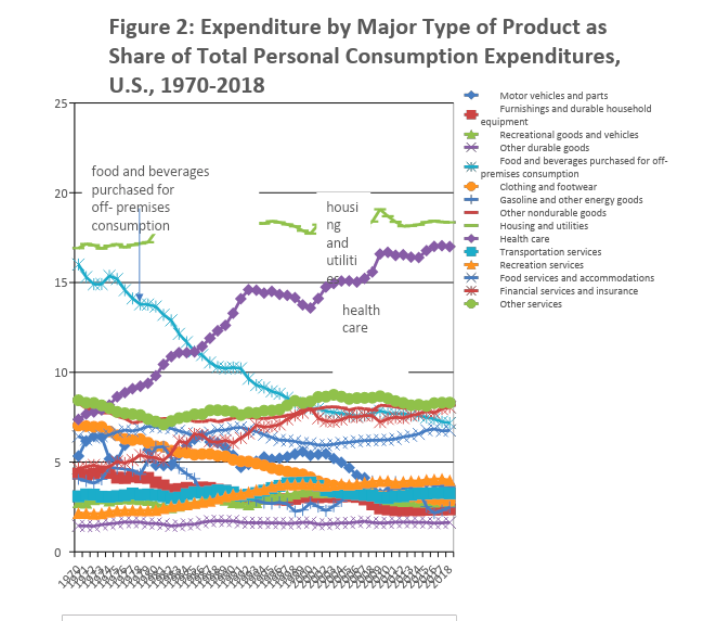

This picture of a trade-off is bolstered when we examine what Americans are actually spending their money on. In the United States, the stereotypical picture of why and how Americans fall into debt blames consumers purchasing flat-screen TVs that they cannot afford; an only slightly less stereotypical picture blames greedy bankers offering subprime mortgages. But over the last decades, Americans have not increased their purchases of luxury goods or housing as a proportion of total consumer spending. Rather, what Americans are spending more money on is health care (Figure 2). Housing is the single most significant item in consumers’ budgets, but this has been the case for decades, as we will discuss further below. Health spending, on the other hand, has risen from less than 8 percent of personal consumption in 1970 to over 17 percent today. Government spending on health care has been steadily rising in the U.S., and particularly since the passage of the Affordable Care Act, public health spending is not particularly low in the U.S. compared to other countries. The main reason American households are nevertheless spending more on health care is because prices are so much higher in the American health care sector. Equivalent amounts of public health spending thus purchase less health in the U.S. than other countries; even private systems of health provision cannot make up the shortfall, and households are left paying out of pocket, to a greater extent than in previous decades, and to a greater extent than in other countries.

Not all countries over all time periods exhibit a trade-off between credit and welfare. For example, in recent years Denmark, Norway, and to some extent Sweden, which all have extensive welfare states, have also seen rising indebtedness as a result of an unusual rise in housing prices alongside low interest rates. Moreover, over the last several decades the United States has become less unusual, as its levels of social insurance have risen and its levels of household indebtedness have fallen, trends that are particularly noticeable under the administration of Barack Obama. But overall, and particularly if we control for other factors that affect credit and welfare, easy credit emerges as an alternative form of the welfare state.