Last December two Democratic representatives, Rosa DeLauro of Connecticut and Jan Schakowsky of Illinois, introduced a health care reform bill called Medicare for America. At the time, it got relatively little publicity, but now that it has been reintroduced as H.R. 2452, it deserves a closer look.

Medicare for America (or M4Am, for short) is increasingly seen as a pragmatic option for Democrats who want to stake out a slightly more centrist position than the party’s progressive superstars. For those with low incomes and chronic illnesses, M4Am, like Senator Bernie Sanders’ Medicare for All, would provide free first-dollar coverage for a wide range of medical, dental, and vision services. Unlike the Sanders plan, though, it would subject people with higher incomes and lower medical expenses to income-based premiums and cost sharing.

Here are some of the key features of M4Am, followed by some suggestions that could further improve its prospects for support from a broad range of the political spectrum.

Medicare for America as Universal Catastrophic Coverage

Medicare for America can be seen as an example of an approach to health care reform known generically as universal catastrophic coverage (UCC). The aim of UCC is to protect everyone against financially ruinous medical expenses though full first-dollar coverage for the poorest and sickest, while requiring income-based cost-sharing from those who can afford it. UCC posits a robust role for the government as a provider of social insurance where needed, while creating adequate scope for market mechanisms where they have the best chance of working.

Within the UCC family, specific plans differ in terms of five key parameters: A low-income cutoff; deductibles; coinsurance and copays; premiums; and specific services exempt from cost sharing. M4Am sets these parameters as follows:

The low-income cutoff. H.R. 2452 sets the low-income cutoff at 200 percent of the federal poverty level (FPL). (As of 2019, the FPL stands at $12,490 for an individual and $25,750 for a family of four.) Households below the cutoff receive coverage free of all premiums and out-of-pocket costs.

Cost sharing. As used here, the term cost sharing refers to the combination of deductibles, coinsurance, and copays that determine the amount that consumers pay out of pocket for services provided. The 2018 version of M4Am included a small deductible, but that has been dropped in H.R. 2452, which relies entirely on coinsurance for cost sharing. The coinsurance rate is set at 20 percent, up to an income-dependent out-of-pocket maximum. For households below 200 percent of the poverty line, the maximum is zero. Above 600 percent, the maximum is $3,500 for an individual and $5,000 for a family. Between those limits, the out-of-pocket maximum varies according to a linear sliding scale.

Coinsurance and deductibles each have their advantages. People subject to deductibles get a stronger market signal to economize on expenditures. On the other hand, for a given out-of-pocket maximum, coinsurance extends over a broader range of spending, so the market signal, although weaker, applies to more transactions. Studies show that both forms of cost sharing sometimes lead consumers to forego appropriate, cost-effective care rather than only avoiding care that is inappropriate or overpriced.

In practice, the amount of spending covered by the M4Am coinsurance formula would depend on both the distribution of income and the distribution of medical expenses among households. Using the U.S. distribution of both variables, my rough estimate is that about 32 percent of all personal medical transactions would be subject to coinsurance, assuming that no transactions were exempt. With a coinsurance rate of 20 percent, that would mean that cost-sharing payments by households would come to about 6.4 percent of all health care spending.

Premiums. Premiums play an important role in the financial model of M4Am. The amount of that each family has to contribute toward premiums would vary with income, as follows:

- Each year the Secretary of Health and Human Services would set a base premium (my term, not used in the law as drafted). The base premium would vary by family size but not by age, health status, or other factors.

- For households below 200 percent of FPL, the premium would be paid in full by M4Am.

- For households in the range of 200 to 600 percent of FPL, the premium would be subsidized. The net premium (that is, the premium less the subsidy) for families in this range would follow a linear scale starting at zero for those at exactly 200 percent of FPL and rising either to the base premium or 8 percent of income, whichever is smaller. Under this formula, the premium is always below 8 percent of income for everyone from 200 percent to 599 percent of FPL.

- For households above 600 percent of FPL, the net premium would top out at 8 percent of income or the base premium, whichever is smaller.

H.R. 2452 is not very specific about how the Secretary would set the base premium. It speaks of “community-rated premiums” which are set “with respect to” the costs of services and administration and do not exceed 8 percent of income for any household. As nearly as I can determine, the intention of M4Am sponsors is that the base premium should be set following actuarial principles that would allow the base premium without subsidies plus cost-sharing to cover the full cost of the program. Premium subsidies would be paid from general revenue.

Exempted services. M4Am, like many other programs, exempts certain services from cost-sharing. Preventive services are one important example, but M4Am does not stop there. Other big-ticket items that would be provided free of coinsurance include long-term services and supports; chronic disease services; services for people with several classes of mental, behavioral, and developmental disabilities; generic drugs and nongenerics where medically necessary; pregnancy services; and emergency services. I am guessing that altogether, more than half of all personal medical spending would be fully exempt from cost sharing.

Financial provisions. The funds needed to cover the costs of premium subsidies and cost-sharing exemptions would come in part from reductions in spending on existing government programs such as Medicaid, the Affordable Care Act (ACA), and the Children’s Health Insurance Program (CHIP). In addition, the bill has several tax provisions, including increased payroll taxes for high-income individuals and for firms that terminate their employee health coverage; a repeal of the Trump tax cut; a 5 percent income tax surcharge on personal incomes over $500,000 per year, and some other items. At some point, someone will need to do a careful financial analysis of the program to see if these sources of funding are adequate, insufficient, or more than adequate.

How Medicare for America Can Reach Its Goals

Health care systems around the world and proposals for reforming the U.S. system vary in terms of the way payments for services are shared between household and nonhousehold sources. The household share for the current U.S. system is about 30 percent, not far above the OECD average of 28 percent. The sponsors of M4Am provide no explicit target, but it is clear they intend to reduce the household share. My own back-of-the-envelope calculations suggest that under M4Am, household payments in the form of premiums and coinsurance fall to something like 20 to 25 percent of all personal medical spending.

I cannot say whether 20 percent, 30 percent, or some other number is optimal. Ultimately, the size of the household contribution is a political decision that would be subject to negotiations as reform plans work their way through Congress. Instead, I would like to focus on some technical suggestions that could help M4Am meet its goals of making health care affordable while asking those who can to pay their fair share, whatever a “fair share” ultimately turns out to be.

Smoothing out the contribution schedules. M4Am calls for household contributions in the form of income-based premiums and coinsurance. However, the contribution schedules that it specifies have some rather quirky properties that might be worth revisiting.

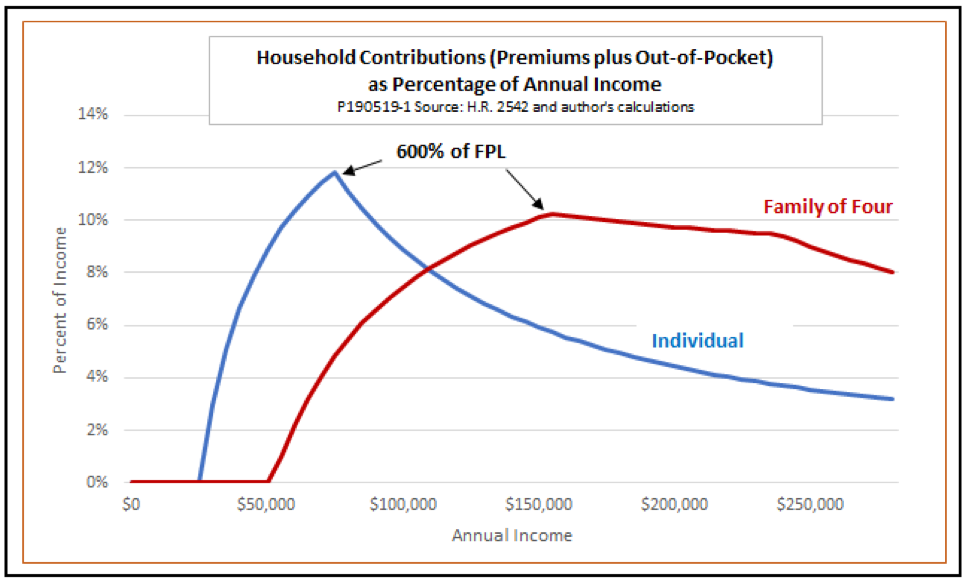

One quirk is that total contributions, including premiums and cost-sharing, hit a maximum as a percentage of income at 600 percent of FPL ($74,940 for an individual or $154,500 for a family of four) and then decrease significantly for upper-middle-class and wealthy households. That remains true even if tax surcharges on high incomes are included along with premiums and coinsurance.

Another quirk arises from the way that income and family size interact as determinants of net premiums. For incomes above 200 percent of FPL, but not very far above that level, large families face a lower maximum contribution as a percentage of income than do individuals or smaller families. However, for families with incomes above 600 percent of FPL or only a little below that level, large families face a higher maximum burden.

Both of these quirks can be seen in the following figure, which shows total maximum household contributions as a percentage of income for individuals and four-member families. For purposes of illustration, the figure assumes base premiums at 120 percent of the 2019 level for ACA silver plans, as given by the Kaiser Family Foundation’s Marketplace Calculator. Actual M4Am premiums could be higher or lower, but the same general patterns would hold.

I do not know if the authors of M4Am specifically intend to give a better deal to more affluent families than to those in the middle class, or to favor larger families in some income ranges and individuals and smaller families in others. Intentional or not, however, I do not find these features especially attractive. Instead, I would suggest a simpler method that would apply income-based contributions more uniformly.

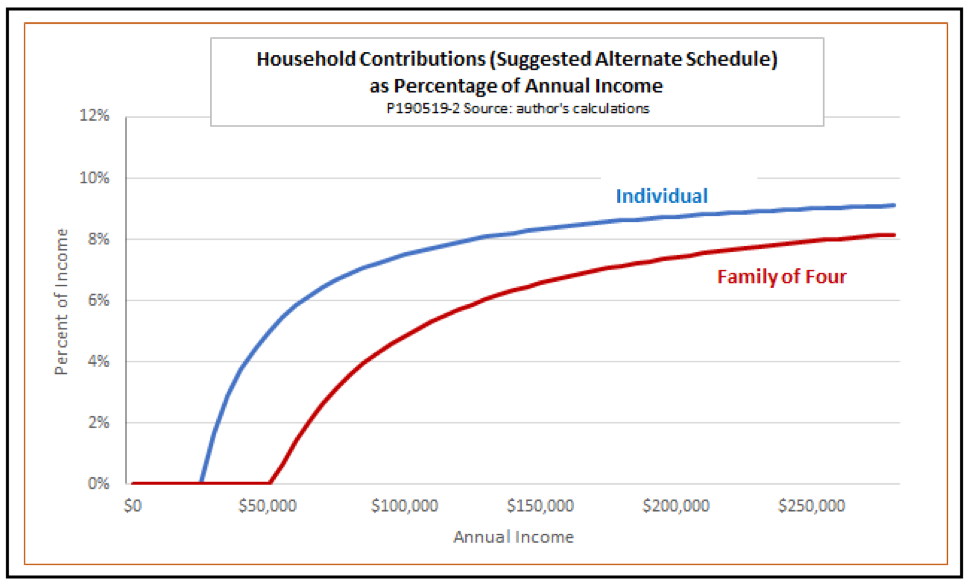

My proposal would set the maximum contribution for all families at a fixed percentage of eligible income, defined as income in excess of the low-income threshold. The following figure gives hypothetical schedules for individuals and four-person families. To keep the numbers close to those used in H.R. 2452, the figure uses 200 percent of FPL as the low-income threshold and sets the maximum household contribution rate at 10 percent, including both premiums and cost sharing:

These alternate schedules apply the principle of income-based contributions uniformly to everyone with middle- and upper incomes. They also ensure that larger families always pay less than smaller ones at any given level of income.

Premiums vs. cost-sharing. Once the overall schedule for household contributions is set, we can turn to the issue of how the total should be divided between premiums and cost sharing. My rough estimate is that the payment schedules proposed in H.R. 2452 would result in a mix consisting of about 85 percent premiums and 15 percent cost sharing.

For a given total household contribution, higher premiums and lower cost sharing tends to shift health care costs, within any income group, away from those who are relatively sick toward those who are relatively healthy. That, in itself, is not unreasonable – after all, such a shift is the whole point of having health insurance in the first place. However, too great a reliance on premiums combined with too little cost sharing has some disadvantages.

One concern is that low cost-sharing requirements reduce the range over which consumers have market incentives to shop carefully for health care. A premium, once paid, is a sunk cost that has no effect on consumers’ decisions to lead a healthy lifestyle, to think twice about nonessential care, or to shop for the best value rather than simply visiting the most convenient provider. True, such incentives are not a cure-all, especially in a system that is as lacking in market transparency and competition as ours is today. However, any proposal that neglects market incentives, or reduces them to a token role, is likely to lose the support of an important segment of the community of health care reformers.

A second concern is that the greater the reliance on premiums, the more acute is the issue of what to do about people who do not pay them. If young, healthy people fail to pay, premiums would rise for those who did participate.

H.R. 2452 leaves it to the HHS Secretary to set appropriate rules concerning nonpayment. Quite possibly those rules might resemble current Medicare rules, which allow disenrollment for nonpayment and impose penalty premium rates on people who later apply for re-enrollment.

Although the existing rules appear to work tolerably well, the problems of nonpayment, disenrollment, and adverse selection might well be more serious under M4Am than they are under traditional Medicare. Partly that is because M4Am premiums are likely to be higher, especially for young, healthy, high-income professionals. Penalties would have to be quite steep to keep nonpayment to an acceptable level.

Also, changes in enrollment status would be more frequent under M4Am than they are for traditional Medicare. Under the current system, enrollment in Medicare, for most people, is a once-in-a-lifetime experience. Under M4Am, many kinds of life events could induce moves onto or off of the program. For example, divorce, death of a spouse, or leaving one’s parents’ household could require a person formerly covered by a family plan to establish an individual policy. For those who remain on employer-sponsored insurance, loss or change of a job could trigger enrollment or re-enrollment in M4Am. There would also be opportunities to move back and forth between M4Am and a proposed Medicare Advantage for America plan, analogous to existing Medicare Advantage plans. Keeping track of who owed what and determining whether lapses in premium payments were due to inadvertence or willful noncompliance would be a major challenge.

Both to enhance incentives for careful shopping and to reduce incentives for nonpayment, I would suggest shifting the revenue mix of M4Am toward lower premiums and higher cost sharing. Without raising the maximum household contribution, that could be done by lowering the base premium while raising the range of spending subject to coinsurance, or by reintroducing a modest deductible (dropped from the 2018 version of M4Am).

Prohibition of private contracting. Another distinctive feature of Medicare for America is an outright ban on private contracting. The relevant language in H.R. 2452 reads as follows:

NO PRIVATE CONTRACTING.—A health care provider or health care institution are prohibited from entering into a private contract with an individual enrolled under Medicare for America for any item or service coverable under Medicare for America.

An official summary of M4Am issued by Rep. DeLauro’s office uses somewhat different language in describing the prohibition:

Medicare for America would fix the current two-tiered healthcare system by banning private contracting. The wealthy and well-connected currently use private contracting to pay for care from providers who do not accept health insurance and demand to be paid completely out of pocket.

Comparing the two versions leaves it unclear whether all private contracting is to be prohibited, or only private contracting with individuals enrolled directly in the basic M4Am plan. Is private contracting prohibited for people who opt out of M4Am because they are enrolled in other qualified coverage, such as employer-sponsored insurance, Medicare Advantage for America, or one of the smaller ongoing government programs such as TRICARE or the Indian Health Service? The language of the bill would appear to say contracting would be prohibited only for those in the basic version while that of the summary implies that the prohibition is universal.

A related issue also needs attention: On the face of it, once M4Am came fully into force, insurance coverage of some kind would be universal. H.R. 2453 specifies that people would be permitted to opt out only if they enroll in other qualified coverage. In practice, however, whether or not coverage was truly universal would also depend on whether people would be disenrolled for nonpayment of premiums. If yes, that would make it possible to opt out of M4Am through the back door, via nonpayment, even without having other eligible coverage. Would providers be allowed to contract with people who had been disenrolled, including those whose disenrollment was intentional? If so, then a two-tier system could very well survive.

In my view, the outright ban on private contracting is unworkable, unnecessary, and undesirable. Instead, I would suggest something like the less restrictive (and more clearly stated) restrictions on contracting found in Section 303 of the Sanders’ Medicare for All bill. That language would be sufficient to prohibit the two most obvious abuses:

- It would outlaw “balance billing,” in which a provider takes the fee offered by government insurance, then bills the patient an additional amount for the same service.

- It would prohibit mixing public and private contracting by a single provider. Among other things, that would eliminate the worry that practitioners with dual practices might rush through a lot of M4Am patients and then take special care with those on private contracts.

As I read it, though, the Sanders language would not prohibit concierge practices that dealt only with private patients and billed the full cost of services to those patients or their private insurers. Although many supporters of single-payer health care do not like private practices of this type, there are good, pragmatic reasons to permit them.

One is that allowing a small private sector would reduce costs of the public program by reducing demand for its services. Anything that reduced the cost of the program without degrading the quality of services, would, in turn, improve its political prospects. The small number of households likely to patronize concierge practices would in no way be free riders on the rest of those served by M4Am. On the contrary. Although they would not pay premiums, if concierge clients had high incomes (as would presumably be the case for most of them), they would still be subject to payroll tax and income tax surcharges. Meanwhile, they would take nothing from M4Am.

Second, the very existence of a small private sector would help to alleviate one of the greatest sources of resistance to universal or near-universal government health care: the fear of long waiting periods. The experience of the British National Health Service provides some lessons in that regard. In the years before Tony Blair became prime minister of the U.K., waiting times in the National Health Service grew alarmingly for procedures like hip replacements. As waits grew longer, the British private sector, normally a small niche market, began to grow. That growth, in turn, acted as a spur to reforms by the Blair government that significantly shortened waiting times. Since then, the private sector has again become smaller.

Conclusions

Medicare for America stands as a welcome addition to the growing number of reform proposals now on the table. It its own way, it adheres to the principles that I have repeatedly urged in previous writings on the reform of health care policy:

- Affordable access to quality care for everyone.

- Freedom from the threat of financially ruinous medical bills.

- Full first-dollar coverage for the very poor and the very sick.

- An expectation that those who can afford it will pay a fair share of the cost of their own care.

- A role for government as a provider of social insurance matched by ample scope for market mechanisms where they work best.

Much more could be said about Medicare for America. For example, I find many of its ideas about transition, the role of employer-sponsored insurance, financing provisions, and other aspects of reform to be well founded. Although there is not room to discuss them here, I have many comments and suggestions regarding those areas, too. I look forward to seeing further development of M4Am as it moves though the legislative process.