Several factors play a critical role in ensuring family economic security. Competitive labor markets create opportunities for families to increase their earning power, while income supplements provide a safety net during times of economic or personal hardship. Evidence also highlights the importance of family structure, showing that children tend to thrive when living in stable, two parent households. However, many parents still face marriage penalties in the tax code, which can work against maintaining this stability.

Marriage penalties occur when a couple’s combined tax liability increases after marriage compared to what they would have paid if they remained single. Research from the Tax Foundation finds two important sources of marriage penalties in the federal tax code are tax brackets that are less than doubled for marriage couples relative to their single counterparts and an Earned Income Tax Credit (EITC) phase out threshold that is less than doubled for marriage couples relative to their single counterparts.

Marriage penalties are not limited to federal taxes. The Tax Foundation also found them embedded in many state income tax brackets. Below, we build on these findings by expanding the scope of potential marriage penalties in state tax codes – particularly for households with children – by examining head of household standard deductions, EITCs, and child tax credits (CTCs). Given the potential benefits of marriage on child well-being, identifying marriage penalties for families is crucial.

State head of household standard deductions

Marriage penalties can be embedded in tax filing status, which determines the standard deduction households can claim to reduce taxable income. Filing status is based on marital status and whether or not there are qualifying dependents. To minimize marriage penalties, tax codes can set the standard deduction for married filers at double the amount for single filers. For example, the IRS recently announced that in 2025, the standard deduction for single filers will be $15,000 and $30,000 for married filers.

However, the federal tax code also provides an additional filing status for single filers with dependents – Head of Household (HoH) – that provides a more generous standard deduction ($22,500 in 2025) relative to single filers without dependents. While HoH status is aimed at providing additional support for single parents, as we have written, it is a flawed mechanism for supporting households with children. One significant issue is that it creates special marriage penalties for single parents.

Many states tie their standard deduction to the federal tax code, including HoH status. In other cases, states set their own standard deduction or do not use one at all, relying instead on personal exemptions alone. Figure 1 shows which states have a HoH standard deduction in their personal income tax codes.

Figure 1. Marriage Penalties in State Head of Household Standard Deductions

Most states have a standard deduction that creates marriage penalties for single parents. Many states that do not have a marriage penalty in their tax brackets still have one in their standard deduction. In Ohio and Virginia, there are no marriage penalties in their standard deduction, but they do exist within their tax brackets.

This picture complicates our view of marriage penalties associated with HoH filing status. Whereas HoH status provides a distinct standard deduction and tax brackets at the federal level, many states have decoupled these elements so that we find marriage penalties in one but not necessarily the other.

State earned income tax credits

The expansion of state EITCs is one of the most successful examples of policy diffusion in recent decades. Since the 1980s, more than half of U.S. states–including one without an income tax– have adopted EITCs. The federal EITC has one of the most well-known marriage penalties for low-income taxpayers, which largely stems from its phaseout thresholds. In 2025, the EITC phaseout threshold will be $23,350 for single parents but only $30,470 for married parents. This disparity can create situations where the decision to marry causes parents to lose some or all of their EITC benefits.

The vast majority of states with an EITC structure them as a percentage of the federal EITC. Three states – California, Washington and Minnesota – have completely distinct EITCs. Figure 2 shows which states with EITCs have embedded marriage penalties.

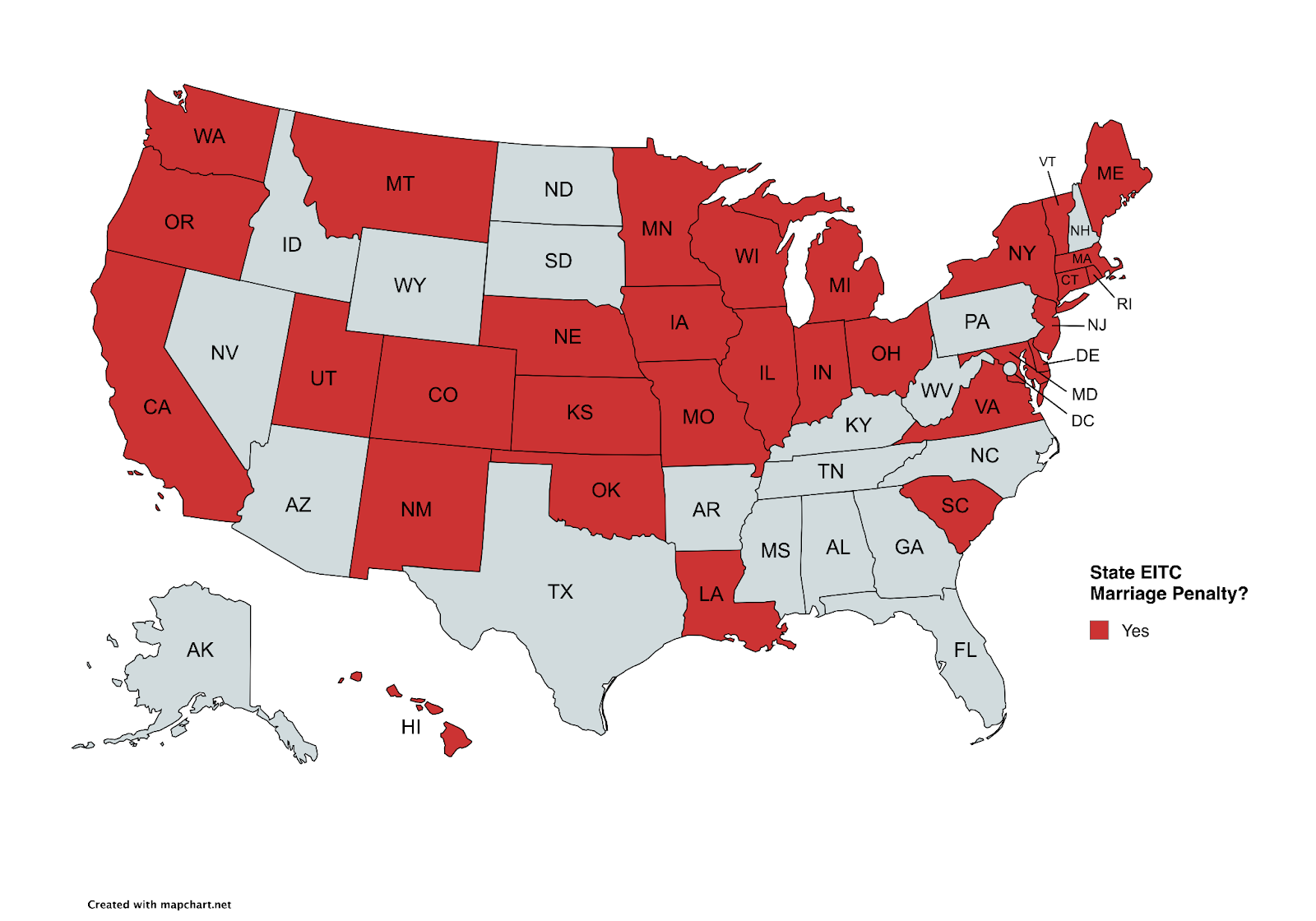

Figure 2. Marriage Penalties in State Earned Income Tax Credits

As you can see, every state EITC includes a marriage penalty, whether the state bases its EITC on a percentage of the federal credit or sets its own independent parameters. States like Washington and Minnesota, with programs like Working Families Tax Credits, have penalties similar to those found in the federal EITC. Meanwhile, California’s CalEITC imposes even more severe marriage penalties.

State child tax credits

State CTCs are a relatively recent policy development, but as of this year, have already been adopted by 20 states. The federal CTC minimizes marriage penalties by doubling the phaseout thresholds for married parents ($400,000) relative to single parents ($200,000).

Unlike the EITC, there is tremendous diversity in the structure of state CTCs. At one end of the spectrum, Massachusetts’ Child and Family Tax Credit does not phase out at all. At the other end, Maryland’s CTC phases out abruptly for any household making more than $15,000. Figure 3 shows which states with CTCs have marriage penalties embedded in their structures.

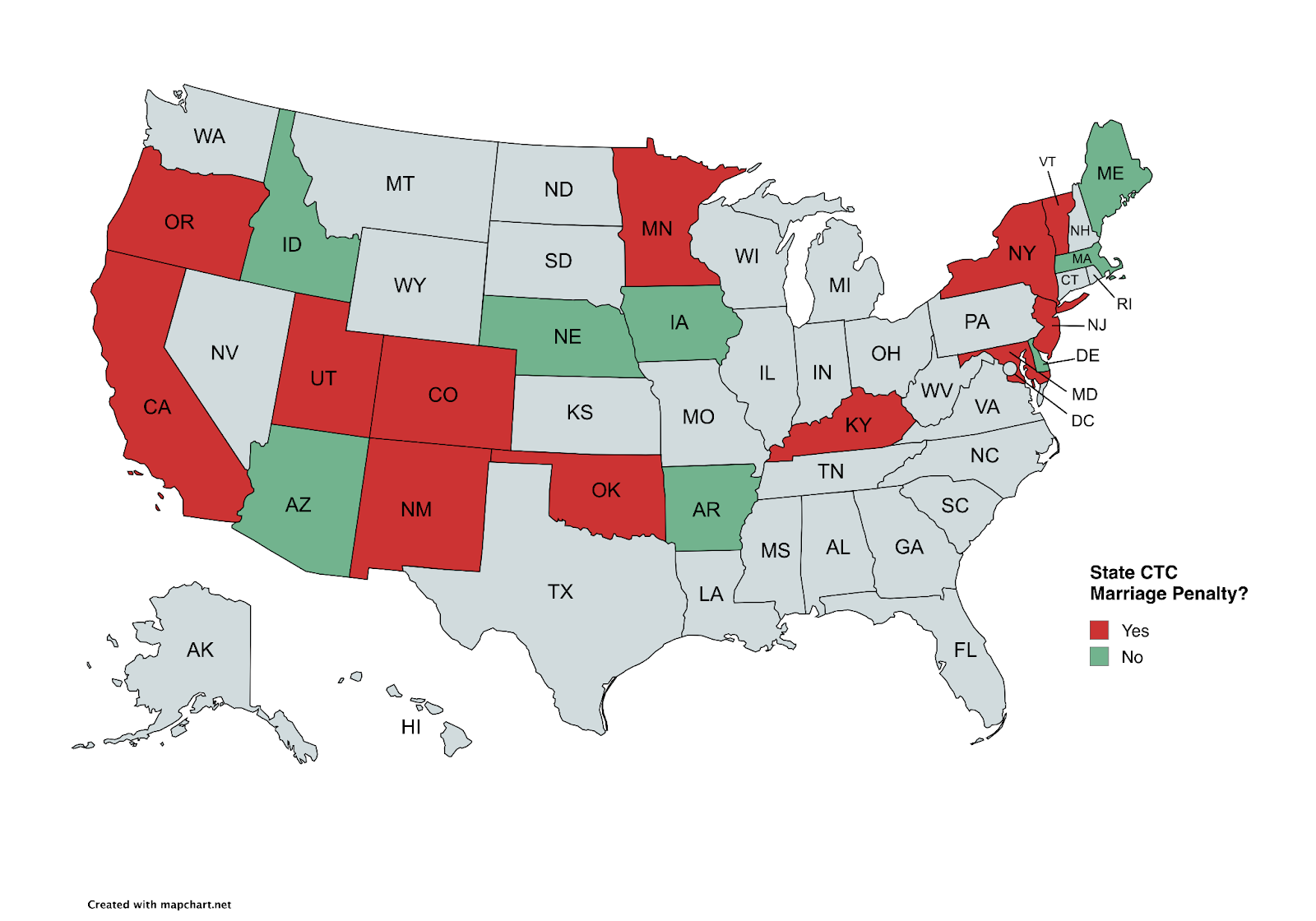

Figure 3. Marriage Penalties in State Child Tax Credits

Most state CTCs have embedded marriage penalties. States that converted personal exemptions into nonrefundable CTCs in the wake of the Tax Cuts and Jobs Act of 2017 are less likely to have marriage penalties, but they are still common. States with refundable CTCs are more likely to have marriage penalties. In many cases, proponents have prioritized poverty impact over other provisions, leading to a focus on hyper-targeting the credit toward those with the lowest incomes. Massachusetts and Maine stand out as the only states with refundable CTCs that avoid marriage penalties. Massachusetts achieves this through the universal nature of its credit, while Maine relies on the federal threshold to minimize penalties.

Time for a federal divorce?

State tax code provisions aimed at supporting families with children, such as HoH standard deductions, EITCs and CTCs, are rife with marriage penalties. Many are the result of state decisions to base portions of their tax code on specific federal provisions that include marriage penalties. Although federal conformity has many advantages, state policymakers should ask themselves whether “conscious uncoupling” makes more sense in cases where conformity means building marriage penalties into their tax code. The case for this is strongest for state HoH standard deductions and EITCs, which cannot avoid marriage penalties as long as they are based on the federal tax code.

While decoupling can mitigate marriage penalties, our findings on state CTCs suggest it’s not a comprehensive solution. Policymakers must carefully design new tax credits to avoid inadvertently recreating these penalties. Identifying the root causes of marriage penalties is a crucial first step for developing effective family support policies.