Noah Smith responded to my piece on Markups and Market Power, both on his own blog and on Twitter. At his personal blog, Noahpinion, he writes

Robin Hanson and Karl Smith both have posts responding to De Loecker and Eeckhout’s paper and attacking the Market Power Story. Both give reasons why they think rising markups indicate monopolistic competition, rather than entry barriers. But both seem to forget that monopolistic competition causes deadweight loss. Just because it has the word “competition” in it does NOT mean that monopolistic competition is efficient. It is not.

Well, let’s talk about that. Now, there is a distinction between partial equilibrium inefficiency and general equilibrium inefficiency. That is, efficiencies that are created in one market can either be exacerbated or ameliorated as they flow through the economy as whole. But I want to set that aside for now. In partial equilibrium analysis, which Noah’s links point to, there are two basic ways in which monopolistic competition is inefficient.

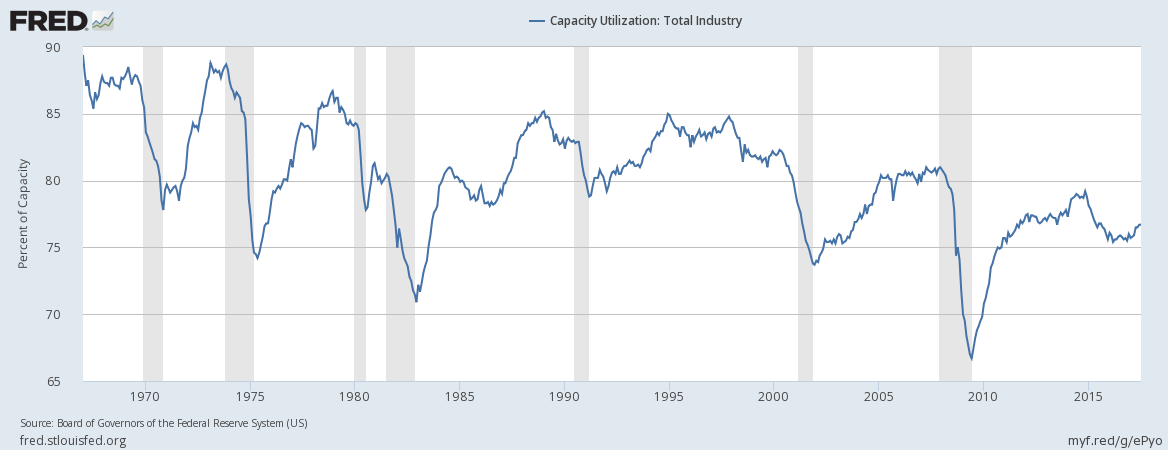

First, monopolistic competition is inefficient because it does not produce at what economists call minimum average total cost. More simply, monopolistically competitive firms do not use their resources as intensely as they could, and they always have a little extra capacity lying around. This is important and is consistent with basic U.S. data trends. Spare capacity has been steadily increasing.

In 1967—the earliest year data is available—capacity utilization in the United States was nearly 90%. It trended steadily downward and today stands at just over 75%. So that’s an element of inefficiency. We essentially have more machines, more storefronts, more factory square footage than we need. Yet, I doubt that’s the kind of inefficiency most folks are thinking about.

The second type of inefficiency that comes out of a partial equilibrium analysis of monopolistic competition is allocative inefficiency. Specifically, monopolistically competitive firms set their prices above their marginal costs. From this stems the most salient fact about monopolistic competition and how one should think about modern economies. That fact is this: monopolistically competitive firms always want to sell more products or services at the market price and will increase their profits if they can find a way to do so.

In contrast, a perfectly competitive firm does not really care one way or the other. They have a product and if you want to buy it, then it buy; if you don’t, then don’t. It doesn’t matter to them one way or another. This is so contradictory to our standard view of business that it’s hard to imagine. It does, however, match the attitude of folks in large agricultural and commodities markets. It also matches the attitude sometimes seen in traditional large open-air markets, with hundreds of sellers, offering homogeneous products. For each seller there is always another customer coming through the bazaar; for each buyer there is always another stall. Wasting your time trying to match with the right seller or attract more buyers yields no return.

Everything that makes modern product markets what they are is related to the fact that matching with the right seller or manufacturer does matter, and attracting and satisfying more customers is at the heart of what it means to do business.

Said another way, what allocative inefficiency pays for in the modern world is customer satisfaction. Indeed one of the hallmarks of monopolistic competition in the abstract is that average firm doesn’t take home especially high profits. That’s because their markup is spent on the very things that differentiate them.

What can happen, however, is that breakout firms—superstars if you will—crack the secret sauce to high satisfaction and mass production. Those firms will earn massive profits on very high markups. This is a lot like the U.S. tech market. But even very successful firms have to keep their eye on the ball in a monopolistically competitive market because failure to maintain customer satisfaction can lead to a swift and certain death.

That, crucially, is what sets monopolistic competition apart from traditional monopolies or cartels. Monopolies and cartels are characteristically lackadaisical. Their customers have little choice and so the companies have little incentive to improve. Their high profits are the result of windfall good fortune or collusion rather than talent, skill, and hard work put into the pursuit of customer satisfaction.

—

Karl Smith is the Director of Economic Research at the Niskanen Center

{kind=link}