Key takeaways

- We explore how American families benefit from two sets of social policies: traditional social assistance programs, including Temporary Assistance for Needy Families (TANF) and the Supplemental Nutrition Assistance Program (SNAP), and refundable tax credits, including Earned Income Tax Credits (EITC) and Child Tax Credits (CTC).

- We evaluate total benefits and implicit marginal tax rates that families with young children face when they increase their earnings. Our analysis focuses on 10 states: California, Colorado, Massachusetts, Maryland, Minnesota, New Jersey, New Mexico, New York, Oregon, and Vermont.

- For families with no earnings, total benefits from social assistance and refundable tax credits ranged from $12,288 in New Mexico to $18,661 in California for a single parent with one child and $20,832 to $29,737 for married parents with two children. These incomes put them between about ⅔ and just short of the federal poverty threshold in 2023.

- In most cases, families face higher implicit marginal tax rates when they move from a minimum to a median wage job than when they transition from welfare to a minimum wage job.

Introduction

Families with young children are potentially eligible for dozens of benefits to support them when they are out of work or to supplement their earnings when they are in work.1 Access to these benefits varies depending on earnings, marital status, age of children, and where families reside. This patchwork across programs and states is so complex that social scientists, advocates, and policymakers often narrow their focus to examine a single program in isolation. While this gives us a clear view of the impact of any one program, we risk missing the forest for the trees.

Families do not experience these programs one at a time, but as an interactive system. In this report, we seek a more holistic understanding of the totality of family benefits, their impact on family resources, and how they support families as their labor market circumstances evolve over time.2 Getting a better, updated understanding of this landscape is particularly important at a time when we are seeing an increasing number of innovative new family benefits in the states.3

This report thus calculates the cumulative impact of six major benefit programs on two types of families and how their benefits change as they move into the labor market and climb the ladder of upward mobility. We find that there are still important reforms that policymakers could enact to ensure families have access to a minimal level of resources while reducing barriers to upward mobility.

We begin with an overview of these programs, with a focus on benefit amounts and program structures. Next, we discuss the states, families, and programs that we model before delving into our main findings. We conclude with key takeaways for policymakers.

America’s family benefit patchwork

Families with children may find themselves benefiting from two sets of social policies that provide them with cash or benefits similar to cash. Traditional social assistance programs include Temporary Assistance for Needy Families (TANF) and the Supplemental Nutrition Assistance Program (SNAP) Both of these are federally supported programs that are administered by states and aimed at supporting families when they’re out of work and attempting to reenter the workforce. Refundable tax credits, which are effectively benefits administered through the tax code, include Earned Income Tax Credits (EITC) and Child Tax Credits (CTC). The federal government and many states independently run their own tax credit programs.

Two aspects of these programs are especially important: the maximum benefit amount and the implicit marginal tax rate (IMTR) they may impose on families. In cases where families receive more than one benefit, these benefits can stack on top of each other, creating a cumulative benefit level much higher than we see for any given program in isolation. The most common example is that families receiving TANF benefits are very likely to be receiving SNAP benefits as well. Evidence suggests that participation in multiple programs is common.4 To fully understand families’ economic standing, we need to know how much they may be receiving in total benefits across multiple programs in any given situation.

We also need to know what kind of work incentives or disincentives they may be facing. Implicit marginal tax rates show us the benefits that families lose (or gain) on each additional dollar of earnings.5 Income-tested programs like TANF, SNAP, and EITC are only available to those with low or moderate earnings. As workers increase their earnings, these benefits begin to phase out, or even abruptly end. The EITC, for example, phases out at a 21.06% rate for each dollar earned after a certain threshold for workers with two children. In other words, they face a 21.06% IMTR on each dollar earned after a certain point.6

In cases where families receive more than one income-tested benefit, these implicit marginal tax rates can likewise stack on top of each other, creating a cumulative IMTRs much higher than we see for any given program in isolation. The most obvious example is the phaseout of state EITCs simultaneously with the federal EITC.

In some cases, workers face “benefit cliffs” where IMTRs climb to 100% and above.7 An additional dollar of earnings may result in workers losing their entire benefit — potentially worth hundreds or thousands of dollars — leaving them worse off than they would have been if they had earned less. Social scientists and policymakers have recognized for decades that high IMTRs are a problem for low-income families with children.

President Nixon was concerned with what he called the “welfare mess” in 1969 when he proposed replacing Aid to Families with Dependent Children (AFDC) (the forerunner of TANF) with an ambitious negative income tax program called the Family Assistance Plan (FAP).8 The problem, as some in his administration saw it, was that AFDC would penalize families trying to move from welfare to work by reducing their benefits 1:1 for each dollar they earned. The FAP was too radical and languished in Congress but spurred renewed attention to the problem of high IMTRs.

Federal policymakers tackled high IMTRs most directly beginning in the 1990s. There was a bipartisan consensus around the need for welfare reform in combination with policies to help “make work pay” for low-income families. Changes to the EITC (1993), AFDC/TANF and SNAP (1996), and the CTC (1997) fundamentally changed the IMTRs facing families making the transition from welfare to work.9 States undertook similar reforms to their TANF and SNAP programs and introduced their own EITCs.

These reforms were largely successful in reducing IMTRs on those moving from welfare to work, but recent evidence suggests that this achievement came at a high cost. Collectively, these reforms shifted the focus of benefits from unemployed households to employed households with low incomes and, in so doing, merely shifted the problem of high IMTRs to households just above the federal poverty level.10

We provide a brief overview of each of these programs today before delving into our analysis.

TANF cash assistance

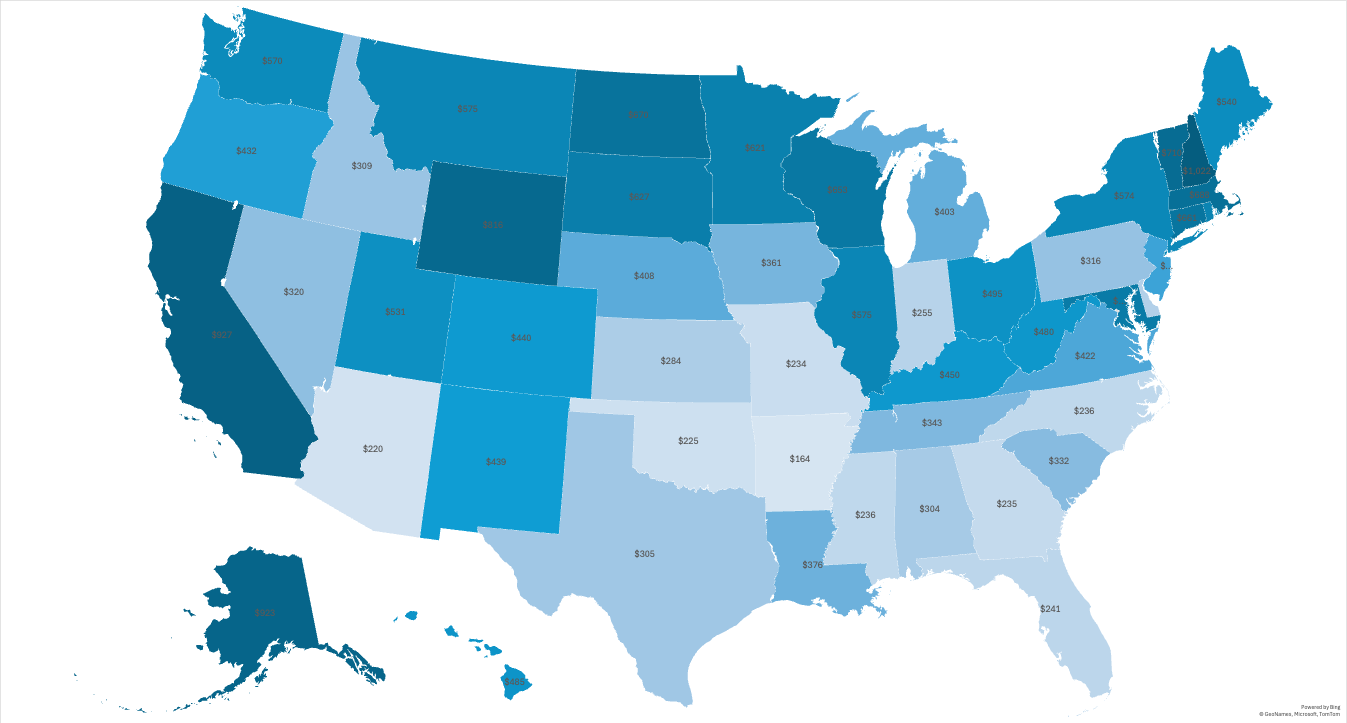

Since the 1996 welfare reforms, TANF has been a state program following broad federal rules and funded partially by federal block grants. Among other benefits, it provides cash assistance to families in need. In 2023, the maximum monthly benefit for a single parent with one child ranged from $164 in Arkansas to $1,022 in New Hampshire (see Figure 1). Many states use a complex combination of earnings disregards and maximum earnings thresholds to create IMTRs that vary widely across states.11

Figure 1: Maximum TANF benefit for a family of two (2023)

The evolution of SNAP

SNAP, formerly known as “food stamps”, is a federal program administered by the states. Initially introduced in 1964, SNAP has evolved into an income-tested near-cash benefit for low-income households. States issue an electronic benefit transfer (EBT) — effectively a debit card for food purchases — to eligible households based on number of members, income, and several other factors. The basic SNAP program has a gross income limit equal to 130% of the federal poverty level (FPL) but most states have taken advantage of the option to expand it to 200% of the FPL by using what is called broad-based categorical eligibility (BBCE).12

The SNAP phaseout rate varies based on a set of income tests and deductions for basic expenses. For most households, this creates IMTRs in the 24-36% range for each additional dollar earned.13 In some cases, households face a benefit cliff where earning an additional dollar can lead to the loss of their entire SNAP benefit. Most states mitigate this cliff effect by using BBCE to provide a longer runway to phase out benefits.

Federal and state EITCs

Congress introduced the federal EITC in 1974 as a temporary measure to help shield lower-income workers with children from rising payroll taxes at the time. It was subsequently made permanent and expanded several times in the decades that followed.

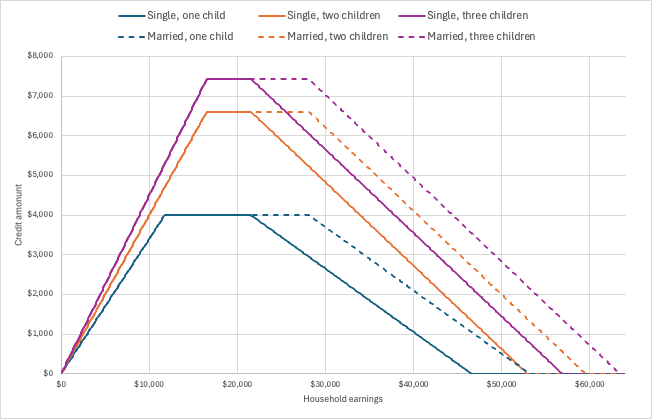

The EITC is a refundable, income-tested tax benefit that phases in with earnings until reaching a maximum benefit ($3,995-$7,430) that varies based on the number of children. It plateaus briefly before phasing out again for single parents earning more than $22,720 and married parents earning more than $29,640. Figure 2 illustrates the value of the EITC for families based on earnings and number of children in 2023.

Figure 2: Value of the federal EITC (2023)

The EITC’s implicit marginal tax rates differ depending on household earnings and number of children. For very low-income families, the IMTR is negative as the credit phases in with earnings. For workers in this range, each additional dollar earned results in an additional 34¢ (one child), 40¢ (two children), or 45¢ (three or more children) in benefits up to a certain amount. They then face a 0% IMTR in the plateau range. After families reach the next earnings threshold, the credit begins to phase out at a rate of either 15.98% (one child) or 21.06% (two or more children).

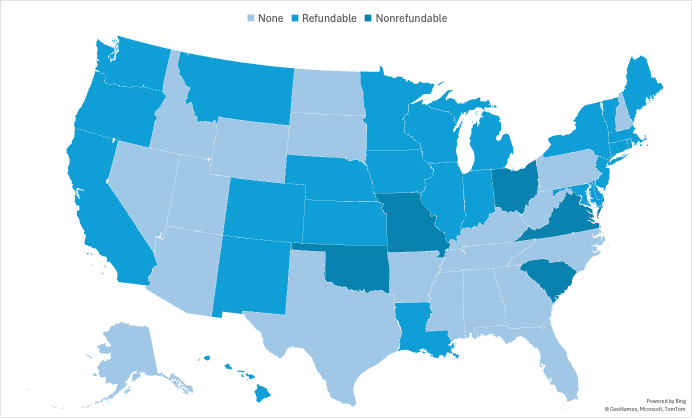

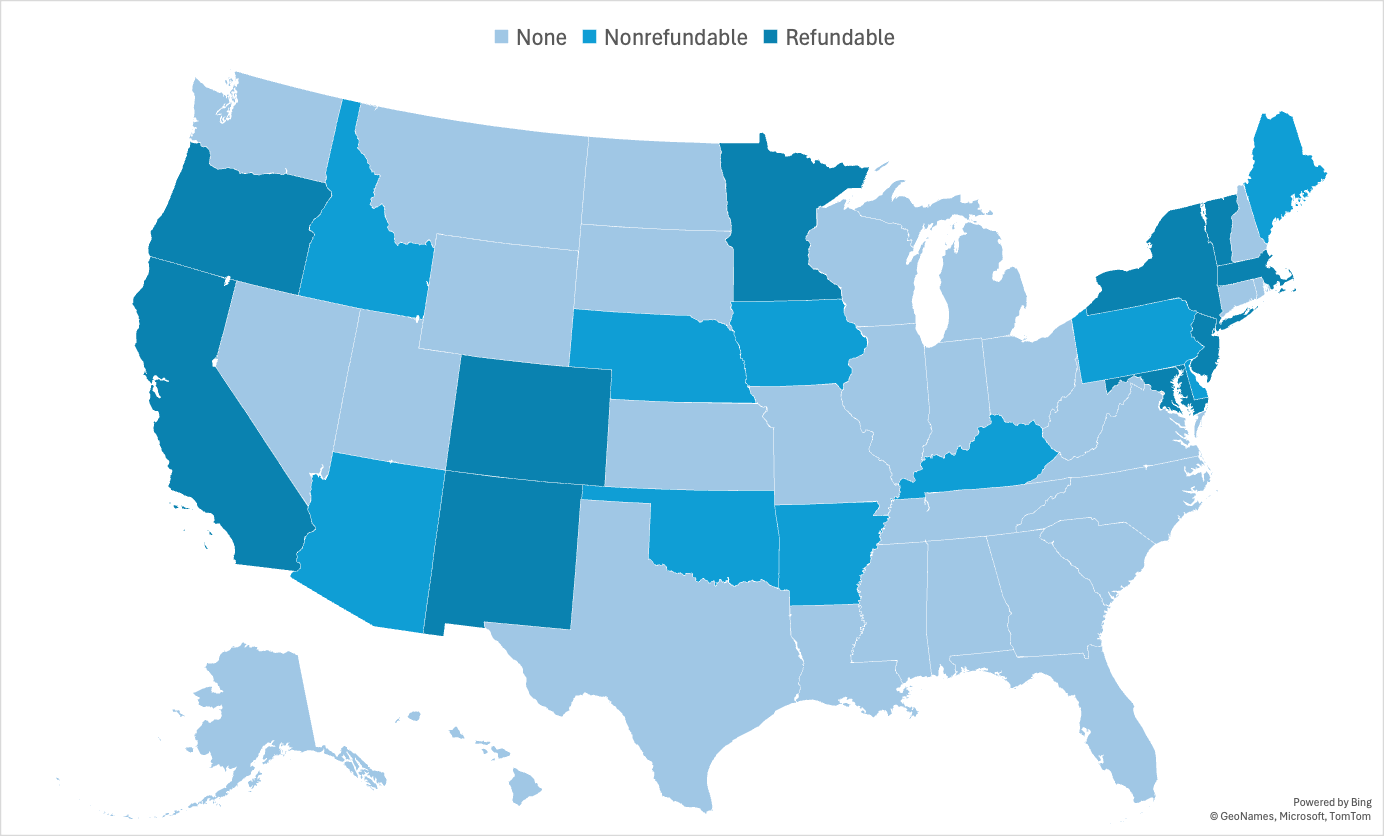

In 1986, Rhode Island became the first state to introduce a state-level EITC. Thirty-two states had their own state-level credits in 2023. All but five states – Missouri, Ohio, Oklahoma, South Carolina, and Utah – provide a refundable credit: If a person’s tax liability is lower than the credit amount they qualify for, the state provides the remainder as a payment.14 Nonrefundable credits can only reduce tax liability to zero. Figure 3 shows states with refundable and nonrefundable credits.

Figure 3: State Earned Income Tax Credits (2023)

Nearly every state sets its EITC at a percentage of the federal credit, with rates ranging from 4 percent in Wisconsin to 125 percent in South Carolina.15 While this results in different credit amounts, states that set their EITC as a percentage of the federal credit adhere to the same threshold structure, which results in varying IMTRs depending on the state’s maximum credit amount.

Federal and state CTCs

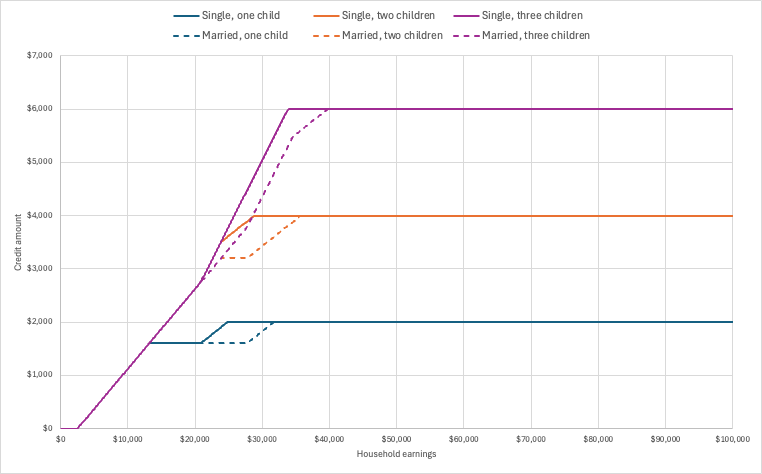

Congress introduced the federal Child Tax Credit in 1997 as a nonrefundable credit for families with children under 17. Over time, Congress increased the value of the credit, the portion that is refundable, and the phaseout thresholds to include more families at the top and bottom. Since 2017, the credit has been worth up to $2,000 per child. It begins to phase out at 5% for single parents making more than $200,000 and married parents making more than $400,000. These IMTRs impact fewer families because they are set so high. Like the EITC, the federal CTC phases in with earnings for low-income families (see figure 4).

Figure 4: Value of the federal CTC (2023)

The first $1,600 of the CTC are refundable and phase in at 15% per household after $2,500 in earnings. Any credit remaining is nonrefundable and phases in depending on a household’s tax liability. Because the $1,600 cutoff for refundability applies even for filers with more than one child, each additional child means the household must have higher earnings (and thus more tax liability) to claim the full credit. As with the EITC, this creates negative IMTRs for low-income families that vary with household size. High-income families face a 5% IMTR as the credit phases out.

Since 2006, 20 states have introduced state-level Child Tax Credits to supplement the federal credit (see figure 5). In 2023, 10 states — California, Colorado, Maryland, Massachusetts, Minnesota, New Jersey, New Mexico, New York, Oregon, and Vermont — provided a fully refundable credit, which makes the full benefit available to families without earnings.16 Maximum benefits range from $310 per child in Massachusetts to $1,750 per child in Minnesota.

Figure 5: State Child Tax Credits (2023)

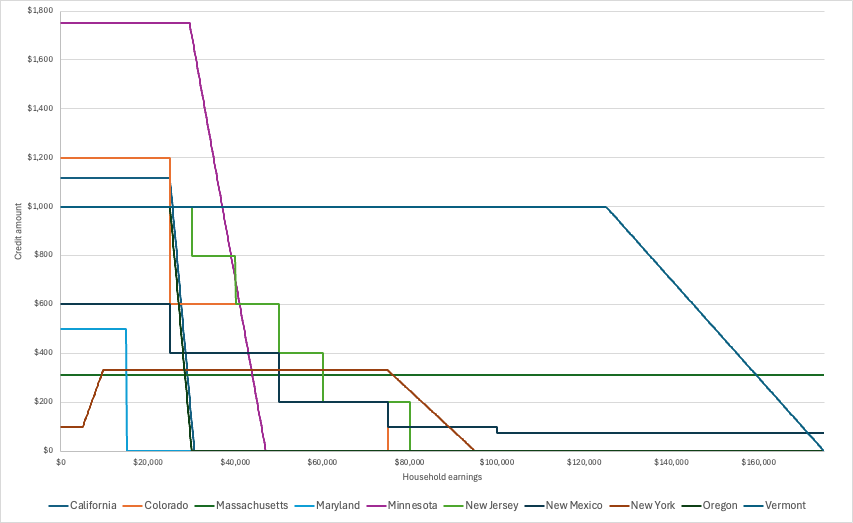

Most states target the credit toward younger children. Age eligibility ranges from children under six years old in six states to children under 17 years old in two states.17 Figure 6 illustrates each state’s CTC structure for a single parent with one young child.

Figure 6: Value of the state CTCs for a single parent with one child (2023)

The most common structure — a fully refundable credit with no phase-in — creates a 0% IMTR for the lowest income families. But states vary widely in terms of phaseout thresholds and rates. Thresholds range from $15,000 in Maryland to Massachusetts’ universal credit. Phaseout rates range from 0% in Massachusetts to benefit cliffs (where earning an additional dollar can result in the loss of all or a substantial amount of the credit) in Colorado, Maryland, New Jersey, and New Mexico. As a result, IMTRs vary widely depending on the state’s credit structure and household earnings.

Measuring benefits and IMTRs for families with young children

We evaluate total benefits and implicit marginal tax rates that families with young children face when they increase their earnings. Our analysis will focus on 10 states: California, Colorado, Massachusetts, Maryland, Minnesota, New Jersey, New Mexico, New York, Oregon, and Vermont. These states were chosen because they all provided a refundable Child Tax Credit in tax year 2023 — a recent innovation that may substantively change what we know about benefits and IMTRs for low-income families.18

We consider six major benefits: TANF, SNAP, federal and state EITCs, and federal and state CTCs. We focus on these six programs because they are the most straightforward cash or near-cash programs that families encounter and — with the exception of TANF — have relatively high take-up rates,19 The impacts of federal and state tax systems more broadly and other means-tested programs warrant further discussion but are beyond the scope of this analysis.

The evaluation will focus on two income zones. We will first explore the benefit changes and IMTRs that arise when families move from welfare to work, which we operationalize as $0 earnings and earnings from working full-time for the relevant state minimum wage. While this transition has been the subject of numerous studies, there is less research on the benefits and IMTRs that upwardly mobile families face when they begin earning beyond the minimum wage. For this reason, we also look at families successfully climbing the economic ladder and changes associated with the transition from a state’s minimum wage to its median wage. Together, these provide us with a more comprehensive picture of total household income (earnings plus benefits) when families advance economically.

Welfare to work: Policymakers tend to focus on the advantages and barriers that arise when families move from welfare to work. We first evaluate the benefits and implicit marginal tax rates that arise when a person with zero income begins working full-time at state minimum wage.20 It is important to look at these rates on a state-by-state basis because minimum wages vary widely between states and may interact with EITCs and CTCs in unexpected ways.21 Some benefits may be phasing in with earnings while others may be phasing out in ways that could potentially affect decision-making, depending on the specific state environment.

Climbing the ladder: Policymakers also often view minimum wage work as a stepping stone that allows low-wage workers to develop their skills, receive raises and promotions, and increase long-run earnings. But, as some evidence suggests, policymakers have inadvertently created new barriers to upward mobility for these same families by pushing them to the phaseout threshold for many means-tested programs. We next evaluate the benefits and implicit marginal tax rates that arise when a household with one parent working full-time at the state minimum wage begins earning the full-time equivalent of the state median wage.22 It was previously unclear whether these families face lower or higher IMTRs than the welfare-to-work families.

We consider two family arrangements: a single parent with one child, age 5, and a married couple with two children, ages 3 and 5. We assume both are single-earner families with one parent working full-time at the state minimum wage, state median wage, or unemployed. We focus on young children because it captures the most crucial years of child development and because parental earnings are typically lower at this stage of life.

We made several additional assumptions when modeling various benefits. Tax credit calculations are relatively straightforward, only requiring adjustment for family size and marital status. For TANF calculations, we assumed that households pay for shelter, have no special needs, and reside in the most populated area of the state. For SNAP, we assumed that no one in the household was over 60 or had a disability and that households did not pay any utilities or monthly homeowners insurance but did pay rent equal to the fair market rent for a two-bedroom in the state’s largest metro (40% of the area’s median rent). For both TANF and SNAP, we assumed that recipients had no unearned or uncounted income like investment income, Social Security, child support, or unemployment benefits.

This approach has important limitations. By focusing exclusively on these benefits, we leave out several other family benefits (e.g., rental assistance, child care assistance, state-level nonrefundable CTCs) as well as traditional tax policies (e.g., payroll taxes, income taxes) that may impact a family’s IMTRs and total disposable income.23 Keeping that in mind, we proceed to our main findings.

Main findings

We provide a brief overview of the findings here and a state-by-state breakdown in the pages that follow.

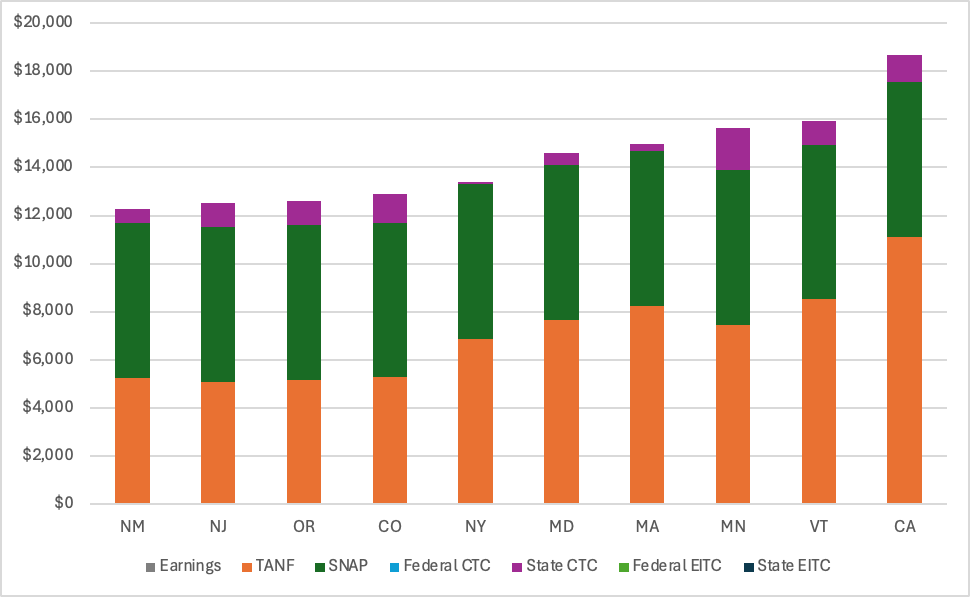

For families with no earnings, total benefits from social assistance and refundable tax credits ranged from $12,288 in New Mexico to $18,661 in California for a single parent with one child and $20,832 to $29,737 for married parents with two children (see figures 7 and 8). Total incomes put these families between about ⅔ and just short of the federal poverty threshold in 2023.

Figure 7: Income breakdown, single parent with one child (unemployed)

Figure 8: Income breakdown, married parents with two children (unemployed)

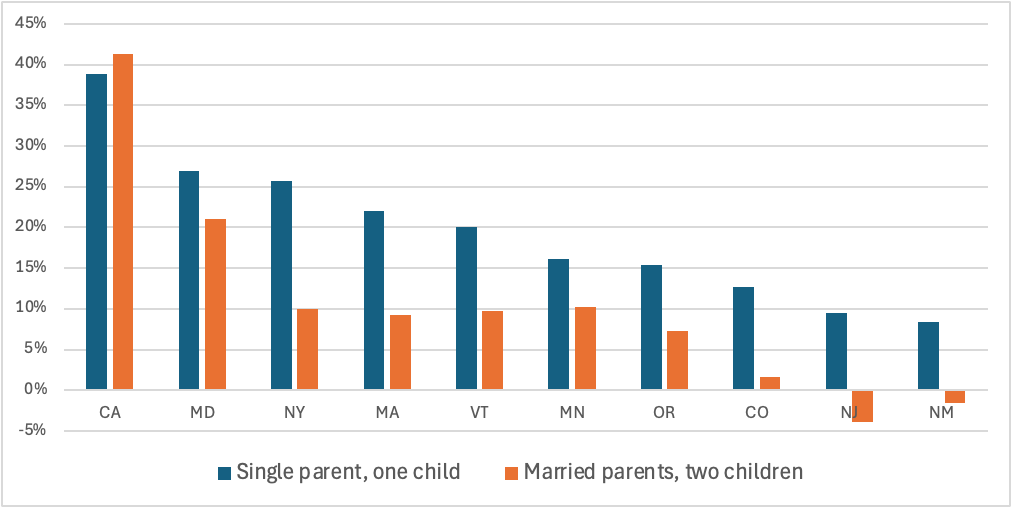

These families face IMTRs ranging from 8.38% in New Mexico to 38.91% in California for a single parent with one child and -3.89% in New Jersey to 41.31% in California for married parents with two children when they move from welfare to work in full-time minimum wage jobs (see Figure 9).

Figure 9: Implicit marginal tax rate on move from welfare to state minimum wage work

Two contributing policy factors help explain this variation, including TANF generosity and state tax credit generosity and structure. More generous TANF benefits tend to lead to higher IMTRs in the transition from welfare to work but more generous state EITC benefits have a countervailing effect. The impact of state CTC benefits varies depending on whether the threshold at which they begin phasing out is low or high. In California, for example, families lose their entire state EITC and CTC when they transition to full-time work.

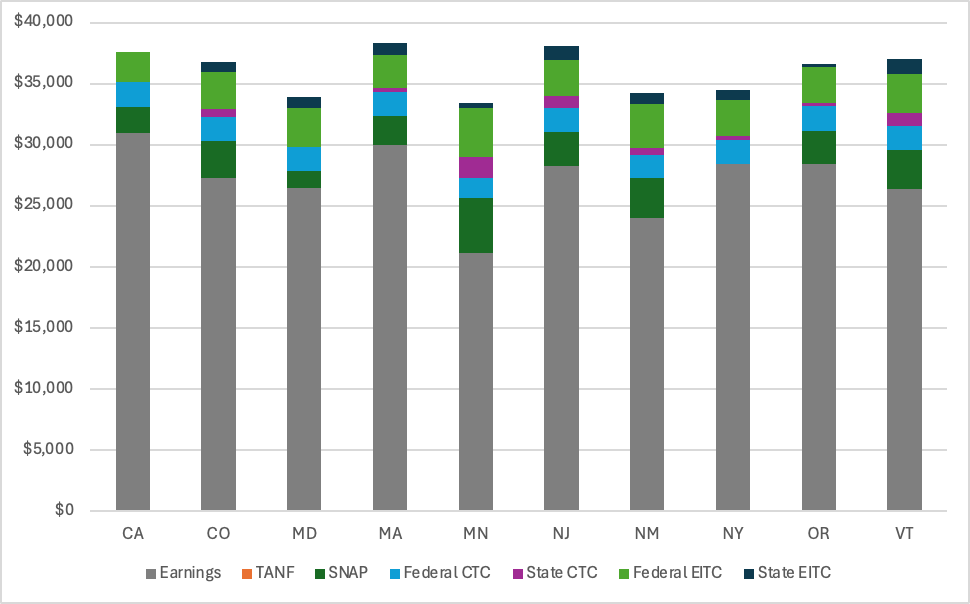

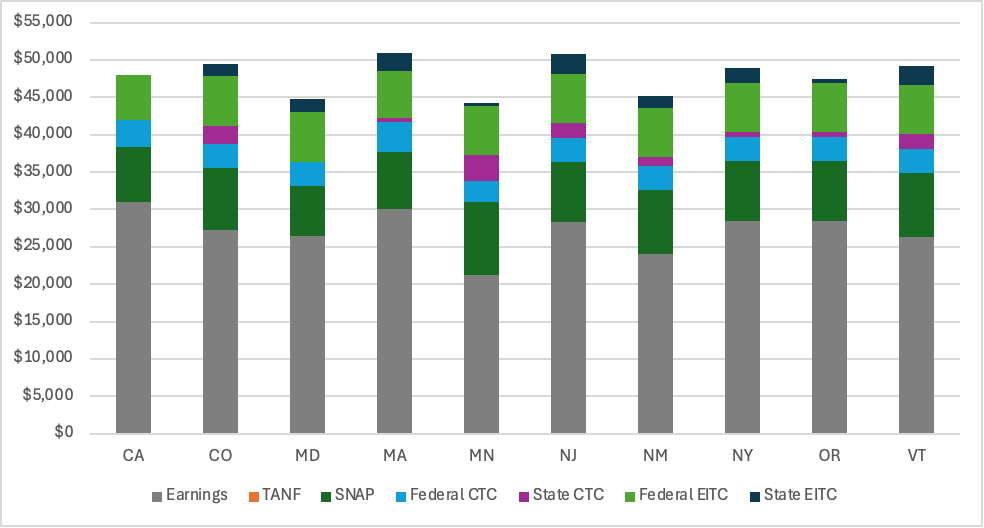

For families where one parent is working full time at the state minimum wage, total income from earnings and the six programs examined here ranged from $33,379 in Minnesota to $38,367 in Massachusetts for a single parent with one child and, in the same two states, $44,195 to $50,995 for married parents with two children (see figures 9 and 10). Total incomes put these families between about 150% and 200% of the federal poverty threshold in 2023.

Figure 10: Income breakdown, single parent with one child (minimum wage)

Figure 11: Income breakdown, married parents with two children (minimum wage)

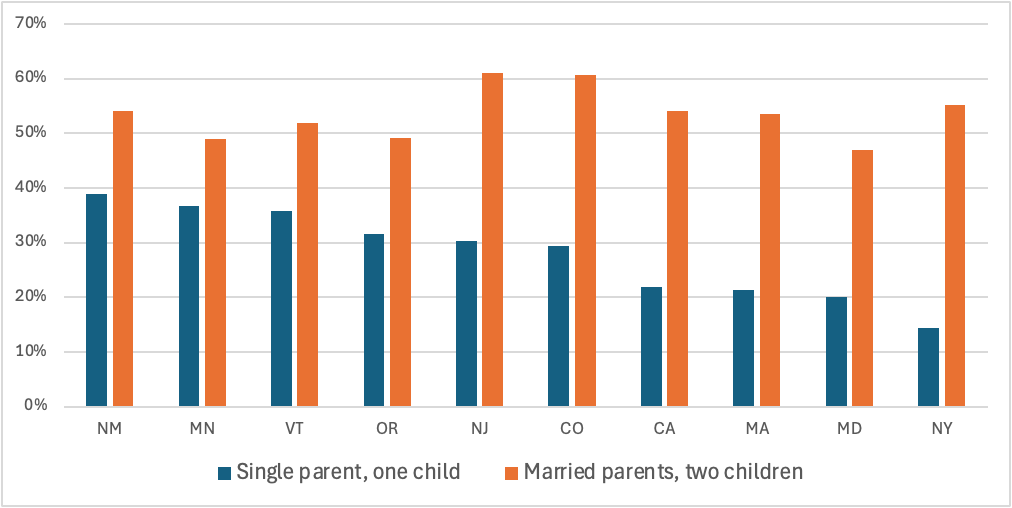

Among those climbing the ladder from full-time minimum wage jobs to median wage jobs, families face IMTRs ranging from 14.37% in New York to 38.84% in New Mexico for a single parent with one child and 46.96% in Maryland to 61.07% in New Jersey for married parents with two children (see Figure 12). These findings confirm previous research that suggests policy reforms have reduced IMTRs at the bottom by pushing them up to families above the federal poverty line.

Figure 12: Implicit marginal tax rate on move from state minimum wage to median wage work

For these families, the concurrent loss of SNAP, federal EITC, state EITC, and state CTCs benefits in some cases contributes to IMTRs that can leave families with less than 50¢ for each additional $1 they earn.

California

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $31,000 | – | $51,960 | – |

| TANF | $11,124 | $0 | 35.88% | $0 | 0.00% |

| SNAP | $6,420 | $2,112 | 13.90% | $0 | 10.08% |

| Federal CTC | $0 | $2,000 | -6.45% | $2,000 | 0.00% |

| State CTC | $1,117 | $0 | 3.60% | $0 | 0.00% |

| Federal EITC | $0 | $2,486 | -8.02% | $0 | 11.86% |

| State EITC | $0 | $0 | 0.00% | $0 | 0.00% |

| Total | $18,661 | $37,598 | 38.91% | $53,960 | 21.94% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $31,000 | – | $51,960 | – |

| TANF | $16,944 | $0 | 54.66% | $0 | 0.00% |

| SNAP | $11,676 | $7,404 | 13.78% | $0 | 35.32% |

| Federal CTC | $0 | $3,530 | -11.39% | $4,000 | -2.24% |

| State CTC | $1,117 | $0 | 3.60% | $0 | 0.00% |

| Federal EITC | $0 | $5,997 | -19.35% | $1,575 | 21.10% |

| State EITC | $0 | $0 | 0.00% | $0 | 0.00% |

| Total | $29,737 | $47,931 | 41.31% | $57,535 | 54.18% |

Colorado

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $27,300 | – | $51,960 | – |

| TANF | $5,280 | $0 | 19.34% | $0 | 0.00% |

| SNAP | $6,420 | $3,000 | 12.53% | $0 | 12.17% |

| Federal CTC | $0 | $2,000 | -7.33% | $2,000 | 0.00% |

| State CTC | $1,200 | $600 | 2.20% | $200 | 1.62% |

| Federal EITC | $0 | $3,078 | -11.27% | $0 | 12.48% |

| State EITC | $0 | $769 | -2.82% | $0 | 3.12% |

| Total | $12,900 | $36,747 | 12.65% | $54,160 | 29.39% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $27,300 | – | $51,960 | – |

| TANF | $8,520 | $0 | 31.21% | $0 | 0.00% |

| SNAP | $11,676 | $8,292 | 12.40% | $0 | 33.63% |

| Federal CTC | $0 | $3,200 | -11.72% | $4,000 | -3.24% |

| State CTC | $2,400 | $2,400 | 0.00% | $1,200 | 4.87% |

| Federal EITC | $0 | $6,604 | -24.19% | $1,575 | 20.39% |

| State EITC | $0 | $1,651 | -6.05% | $394 | 5.10% |

| Total | $22,596 | $49,447 | 1.64% | $59,129 | 60.74% |

Maryland

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $26,500 | $53,660 | ||

| TANF | $7,680 | $0 | 28.98% | $0 | 0.00% |

| SNAP | $6,420 | $1,344 | 19.15% | $0 | 4.95% |

| Federal CTC | $0 | $2,000 | -7.55% | $2,000 | 0.00% |

| State CTC | $500 | $0 | 1.89% | $0 | 0.00% |

| Federal EITC | $0 | $3,206 | -12.10% | $0 | 11.80% |

| State EITC | $0 | $898 | -3.39% | $0 | 3.31% |

| Total | $14,600 | $33,948 | 26.99% | $55,660 | 20.06% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $26,500 | – | $53,660 | – |

| TANF | $11,220 | $0 | 42.34% | $0 | 0.00% |

| SNAP | $11,676 | $6,660 | 18.93% | $0 | 24.52% |

| Federal CTC | $0 | $3,200 | -12.08% | $4,000 | -2.95% |

| State CTC | $1,000 | $0 | 3.77% | $0 | 0.00% |

| Federal EITC | $0 | $6,604 | -24.92% | $1,217 | 19.83% |

| State EITC | $0 | $1,849 | -6.98% | $341 | 5.55% |

| Total | $23,896 | $44,813 | 21.07% | $59,218 | 46.96% |

Massachusetts

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $30,000 | $58,360 | ||

| TANF | $8,256 | $0 | 27.52% | $0 | 0.00% |

| SNAP | $6,420 | $2,352 | 13.56% | $0 | 8.29% |

| Federal CTC | $0 | $2,000 | -6.67% | $2,000 | 0.00% |

| State CTC | $310 | $310 | 0.00% | $310 | 0.00% |

| Federal EITC | $0 | $2,646 | -8.82% | $0 | 9.33% |

| State EITC | $0 | $1,059 | -3.53% | $0 | 3.73% |

| Total | $14,986 | $38,367 | 22.06% | $60,670 | 21.36% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $30,000 | – | $58,360 | – |

| TANF | $11,424 | $0 | 38.08% | $0 | 0.00% |

| SNAP | $11,676 | $7,644 | 13.44% | $828 | 24.03% |

| Federal CTC | $0 | $4,000 | -13.33% | $4,000 | 0.00% |

| State CTC | $620 | $620 | 0.00% | $620 | 0.00% |

| Federal EITC | $0 | $6,208 | -20.69% | $227 | 21.09% |

| State EITC | $0 | $2,483 | -8.28% | $91 | 8.43% |

| Total | $23,720 | $50,955 | 9.22% | $64,126 | 53.56% |

Minnesota

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $21,180 | $48,920 | ||

| TANF | $7,452 | $0 | 35.18% | $0 | 0.00% |

| SNAP | $6,420 | $4,464 | 9.24% | $0 | 16.09% |

| Federal CTC | $0 | $1,640 | -7.74% | $2,000 | -1.30% |

| State CTC | $1,750 | $1,750 | 0.00% | $0 | 6.31% |

| Federal EITC | $0 | $3,995 | -18.86% | $0 | 14.40% |

| State EITC | $0 | $350 | -1.65% | $0 | 1.26% |

| Total | $15,622 | $33,379 | 16.16% | $50,920 | 36.77% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $21,180 | – | $48,920 | – |

| TANF | $9,996 | $0 | 47.20% | $0 | 0.00% |

| SNAP | $11,676 | $9,756 | 9.07% | $1,032 | 31.45% |

| Federal CTC | $0 | $2,805 | -13.24% | $4,000 | -4.31% |

| State CTC | $3,500 | $3,500 | 0.00% | $1,984 | 5.47% |

| Federal EITC | $0 | $6,604 | -31.18% | $2,228 | 15.78% |

| State EITC | $0 | $350 | -1.65% | $198 | 0.55% |

| Total | $25,172 | $44,195 | 10.18% | $58,362 | 48.93% |

New Jersey

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $28,260 | – | $52,760 | – |

| TANF | $5,100 | $0 | 18.05% | $0 | 0.00% |

| SNAP | $6,420 | $2,760 | 12.95% | $0 | 11.27% |

| Federal CTC | $0 | $2,000 | -7.08% | $2,000 | 0.00% |

| State CTC | $1,000 | $1,000 | 0.00% | $400 | 2.45% |

| Federal EITC | $0 | $2,918 | -10.33% | $0 | 11.91% |

| State EITC | $0 | $1,167 | -4.13% | $0 | 4.76% |

| Total | $12,520 | $38,105 | 9.47% | $55,160 | 30.39% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $28,260 | – | $52,760 | – |

| TANF | $7,728 | $0 | 27.35% | $0 | 0.00% |

| SNAP | $11,676 | $8,052 | 12.82% | $684 | 30.07% |

| Federal CTC | $0 | $3,260 | -11.54% | $4,000 | -3.02% |

| State CTC | $2,000 | $2,000 | 0.00% | $800 | 4.90% |

| Federal EITC | $0 | $6,566 | -23.23% | $1,406 | 21.06% |

| State EITC | $0 | $2,626 | -9.29% | $653 | 8.05% |

| Total | $21,404 | $50,764 | -3.89% | $60,303 | 61.07% |

New Mexico

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $24,000 | – | $41,940 | – |

| TANF | $5,268 | $0 | 21.95% | $0 | 0.00% |

| SNAP | $6,420 | $3,252 | 13.20% | $0 | 18.13% |

| Federal CTC | $0 | $1,920 | -8.00% | $2,000 | -0.45% |

| State CTC | $600 | $600 | 0.00% | $400 | 1.11% |

| Federal EITC | $0 | $3,605 | -15.02% | $729 | 16.03% |

| State EITC | $0 | $901 | -3.75% | $182 | 4.01% |

| Total | $12,288 | $34,278 | 8.38% | $45,251 | 38.84% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $24,000 | – | $41,940 | – |

| TANF | $7,956 | $0 | 33.15% | $0 | 0.00% |

| SNAP | $11,676 | $8,556 | 13.00% | $2,112 | 35.92% |

| Federal CTC | $0 | $3,200 | -13.33% | $4,000 | -4.46% |

| State CTC | $1,200 | $1,200 | 0.00% | $800 | 2.23% |

| Federal EITC | $0 | $6,604 | -27.52% | $3,681 | 16.29% |

| State EITC | $0 | $1,651 | -6.88% | $920 | 4.07% |

| Total | $20,832 | $45,211 | -1.58% | $53,453 | 54.06% |

New York

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $28,400 | – | $54,660 | – |

| TANF | $6,888 | $0 | 24.25% | $0 | 0.00% |

| SNAP | $6,420 | $0 | 22.61% | $0 | 0.00% |

| Federal CTC | $0 | $2,000 | -7.04% | $2,000 | 0.00% |

| State CTC | $100 | $330 | -0.81% | $330 | 0.00% |

| Federal EITC | $0 | $2,902 | -10.22% | $0 | 11.05% |

| State EITC | $0 | $871 | -3.07% | $0 | 3.32% |

| Total | $13,408 | $34,503 | 25.72% | $56,990 | 14.37% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $28,400 | – | $54,660 | – |

| TANF | $11,412 | $0 | 40.18% | $0 | 0.00% |

| SNAP | $11,676 | $8,028 | 12.85% | $0 | 30.57% |

| Federal CTC | $0 | $3,270 | -11.51% | $4,000 | -2.78% |

| State CTC | $200 | $660 | -1.62% | $660 | 0.00% |

| Federal EITC | $0 | $6,545 | -23.05% | $1,006 | 21.09% |

| State EITC | $0 | $1,964 | -6.92% | $302 | 6.33% |

| Total | $23,288 | $48,867 | 9.93% | $60,628 | 55.21% |

Oregon

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $28,400 | – | $48,080 | – |

| TANF | $5,184 | $0 | 18.25% | $0 | 0.00% |

| SNAP | $6,420 | $2,736 | 12.97% | $0 | 13.90% |

| Federal CTC | $0 | $2,000 | -7.04% | $2,000 | 0.00% |

| State CTC | $1,000 | $320 | 2.39% | $0 | 1.63% |

| Federal EITC | $0 | $2,902 | -10.22% | $0 | 14.75% |

| State EITC | $0 | $261 | -0.92% | $0 | 1.33% |

| Total | $12,604 | $36,619 | 15.44% | $50,080 | 31.60% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $28,400 | – | $48,080 | – |

| TANF | $7,452 | $0 | 26.24% | $0 | 0.00% |

| SNAP | $11,676 | $8,028 | 12.85% | $2,772 | 26.71% |

| Federal CTC | $0 | $3,270 | -11.51% | $4,000 | -3.71% |

| State CTC | $2,000 | $640 | 4.79% | $0 | 3.25% |

| Federal EITC | $0 | $6,545 | -23.05% | $2,396 | 21.08% |

| State EITC | $0 | $589 | -2.07% | $216 | 1.90% |

| Total | $21,128 | $47,472 | 7.24% | $57,464 | 49.23% |

Vermont

Single parent, one child (age 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $26,360 | – | $47,720 | – |

| TANF | $8,520 | $0 | 32.32% | $0 | 0.00% |

| SNAP | $6,420 | $3,216 | 12.15% | $0 | 15.06% |

| Federal CTC | $0 | $2,000 | -7.59% | $2,000 | 0.00% |

| State CTC | $1,000 | $1,000 | 0.00% | $1,000 | 0.00% |

| Federal EITC | $0 | $3,222 | -12.22% | $0 | 15.08% |

| State EITC | $0 | $1,224 | -4.64% | $0 | 5.73% |

| Total | $15,940 | $37,022 | 20.02% | $50,720 | 35.87% |

Married parent, two children (ages 3 and 5)

| No earnings | Full-time at state minimum wage | Full-time at state median wage | |||

| Income | Income | IMTR | Income | IMTR | |

| Earnings | $0 | $26,360 | – | $47,720 | – |

| TANF | $11,712 | $0 | 44.43% | $0 | 0.00% |

| SNAP | $11,676 | $8,508 | 12.02% | $2,316 | 28.99% |

| Federal CTC | $0 | $3,200 | -12.14% | $4,000 | -3.75% |

| State CTC | $2,000 | $2,000 | 0.00% | $2,000 | 0.00% |

| Federal EITC | $0 | $6,604 | -25.05% | $2,480 | 19.31% |

| State EITC | $0 | $2,510 | -9.52% | $943 | 7.34% |

| Total | $25,388 | $49,182 | 9.73% | $59,459 | 51.89% |

Conclusion

Policymakers often find themselves thinking about the tradeoff between maximizing the anti-poverty and pro-work impact of a family benefit in isolation. But, as we find, the picture is much more complicated because of benefit interactions that these policy’s architects may not have considered during previous reform episodes. This endeavor is made even harder by the fact that federal and state policymakers are making separate decisions under very different circumstances.

The goal of our initial analysis is to provide policymakers with a more comprehensive picture of family benefits in America. Our family-centered perspective provides a more holistic understanding of the totality of family benefits and how they support families as their labor market circumstances evolve over time.

We hope state and federal policymakers use these findings to undertake more comprehensive reforms that get more parents into employment so they become self-sufficient without eroding benefits for temporarily unemployed parents and their children.

About the authors

Joshua McCabe is the Director of Social Policy. He focuses on issues related to child poverty and household stability. McCabe previously worked as an Assistant Professor of Sociology and Assistant Dean for Social Sciences at Endicott College. McCabe’s work has been featured in the Washington Post, National Review, The Hill, and more. McCabe received his B.A. in Political Science from Emmanuel College, his M.A. in Regional Economic and Social Development from the University of Massachusetts, Lowell, and his Ph.D. in Sociology from the State University of New York at Albany.

Julia Pelletier is a former intern with the Niskanen Center’s social policy team. She is a senior in the Gerald R. Ford School of Public Policy at the University of Michigan. Her coursework and professional experiences focus on social policy, fiscal sustainability, and the effects of poverty on criminal justice issues.

Footnotes

- U.S. House. “Welfare Reform at 20: The Challenges with Reforming the Rest of the Welfare System” (Washington DC: Committee on Ways and Means, 2016). ↩︎

- For similar approaches, see the excellent work of Jennifer Romich, including but not limited to “Difficult Calculations: Low-Income Workers and Marginal Tax Rates,” Social Service Review 80, No. 1 (2006); Prenatal-to-3 Policy Impact Center’s 2023 Policy Impact Calculator; and Eugene Steuerle’s testimony “Marginal Tax Rates, Work, and the Nation’s Real Tax System.” ↩︎

- Joshua McCabe, “The state of our families: Child and dependent tax benefits in the states” (Washington D.C.: Niskanen Center, 2023) ↩︎

- Suzanne Macartney and Robin Ghertner, “How Many People that Receive One Safety Net Benefit Also Receive Others?” (Washington DC: Office of the Assistant Secretary for Planning and Evaluation, U.S. Department of Health and Human Services, 2023). ↩︎

- See briefs in the Assistant Secretary for Planning and Evaluation’s Marginal Tax Rate Series (2019). ↩︎

- Margot Crandall-Hollick, Gene Falk, and Conor Boyle, The Earned Income Tax Credit (EITC): How It Works and Who Receives It (Washington, D.C.: Congressional Research Service, 2023) ↩︎

- Teresa Anderson et al, “Balancing at the Edge of the Cliff Experiences and Calculations of Benefit Cliffs, Plateaus, and Trade-Offs” (Washington D.C.: Urban Institute, 2022); Kess Ballentine,, Sara Goodkind, and Jeffrey Shook. “How Low-Paid Parents Navigate The Complex Financial Landscape Of Benefits Cliffs And Disincentive Deserts,” Health Affairs 41, no. 12 (2022); Craig Richardson and Zachary Blizard, “Benefits cliffs, disincentive deserts, and economic mobility,” Journal of Poverty 26, no. 1 (2022); National Council of State Legislatures, Moving on Up Helping Families Climb the Economic Ladder by Addressing Benefits Cliffs (Washington, D.C.: NCSL, 2019). ↩︎

- Brian Steensland, The Failed Welfare Revolution: America’s Struggle over Guaranteed Income Policy (Princeton: Princeton University Press, 2018). ↩︎

- Joshua McCabe, The Fiscalization of Social Policy: How Taxpayers Trumped Children in the Fight Against Child Poverty (Oxford University Press, 2018). ↩︎

- Robert Moffitt, “The deserving poor, the family, and the US welfare system,” Demography 52, No. 3 (2015); Elaine Maag, Eugene Steuerle, Ritadhi Chakravarti, and Caleb Quakenbush, “How marginal tax rates affect families at various levels of poverty,” National Tax Journal 65, no. 4 (2012); Assistant Secretary for Planning and Evaluation (2019) “Marginal Tax Rate Series”; Ed Dolan, Work disincentives hit the near-poor hardest. Why and what to do about it. (Washington, D.C.: Niskanen Center, 2022); Zachary Parolin, Matthew Desmond, and Christopher Wimer, “Inequality Below the Poverty Line since 1967: The Role of the U.S. Welfare State,” American Sociological Review 88, no. 5 (2023). ↩︎

- See Urban Institute’s Welfare Rules Databook; Gene Falk, Temporary Assistance for Needy Families: The Decline in Assistance Receipt Among Eligible Individuals (Washington D.C.: Congressional Research Service, 2023). ↩︎

- Craig Gundersen, Timothy Smeeding, Judith Bartfeld, and James Ziliak, SNAP Matters: How Food Stamps Affect Health and Well-Being (Stanford: Stanford University Press, 2015); Randy Aussenberg and Gene Falk, Supplemental Nutrition Assistance Program (SNAP): A Primer on Eligibility and Benefits (Washington D.C.: Congressional Research Service, 2023). ↩︎

- Joseph Llobrera and Lauren Hall, “SNAP Provides Critical Benefits to Workers and Their Families” (Washington D.C.: Center on Budget and Policy Priorities, 2023). ↩︎

- Delaware and Maryland allow filers to choose between a more generous nonrefundable credit or a less generous refundable credit. ↩︎

- California, Minnesota, and Washington set their own parameters. See National Council of State Legislatures, Earned Income Tax Credit Overview (Washington D.C.: NCSL, 2024). ↩︎

- Maine became the 11th state in 2023, but the law does not take effect until 2024. ↩︎

- Joshua McCabe, The state of our families: Child and dependent tax benefits in the states (Washington D.C.: Niskanen Center, 2023); Halah Ahmad and Jack Landry, Cash at the State Level: Guaranteed Income Through the Child Tax Credit (New York: Jain Family Institute, 2023); Aiden Davis and Neva Butkus, States are Boosting Economic Security with Child Tax Credits in 2023 (Washington D.C.: Institute on Taxation and Economic Policy, 2023). ↩︎

- We are indebted to and building on the earlier work of Steuerle and Romich in the United States and the Caledon Institute in Canada. See Jennefer Laidley and Mohy-Dean Tabbara, Welfare in Canada, 2023 (Toronto: Maytree/Caledon Institute, 2024). ↩︎

- Despite steadily declining access to TANF cash assistance, it is still considered one of the major social assistance programs for unemployed families with children so we include it here. ↩︎

- U.S. Department of Labor, Changes in Basic Minimum Wages in Non-Farm Employment Under State Law: Selected Years 1968 to 2023 (Washington D.C.: Division of Fair Labor Standards Act and Child Labor, 2024). ↩︎

- Joshua McCabe, “Stop trying to increase state minimum wages and EITCs – and focus on state CTCs” (Washington D.C.: Niskanen Center, 2024). ↩︎

- U.S. Department of Labor, “May 2023 State Occupational Employment and Wage Estimates” (Washington D.C.: Bureau of Labor Statistics, 2024). ↩︎

- For a more comprehensive treatment of the issues related to measuring IMTRs, see Sebastian Leguizamon, “Estimating implicit marginal tax rates of welfare recipients across the US states,” Public Finance Review 40, no. 3 (2012). ↩︎